How to Set Up and Implement Profit First Accounts for Australian Businesses

- Najma Khan

- 2 days ago

- 4 min read

If you’ve ever looked at your bank balance and wondered,

“How can my business be making good money but I still feel broke?”

you’re not alone.

It’s one of the most common frustrations business owners face. Revenue is growing, clients are coming in, and yet there never seems to be enough cash left over for you, for tax, or for profit.

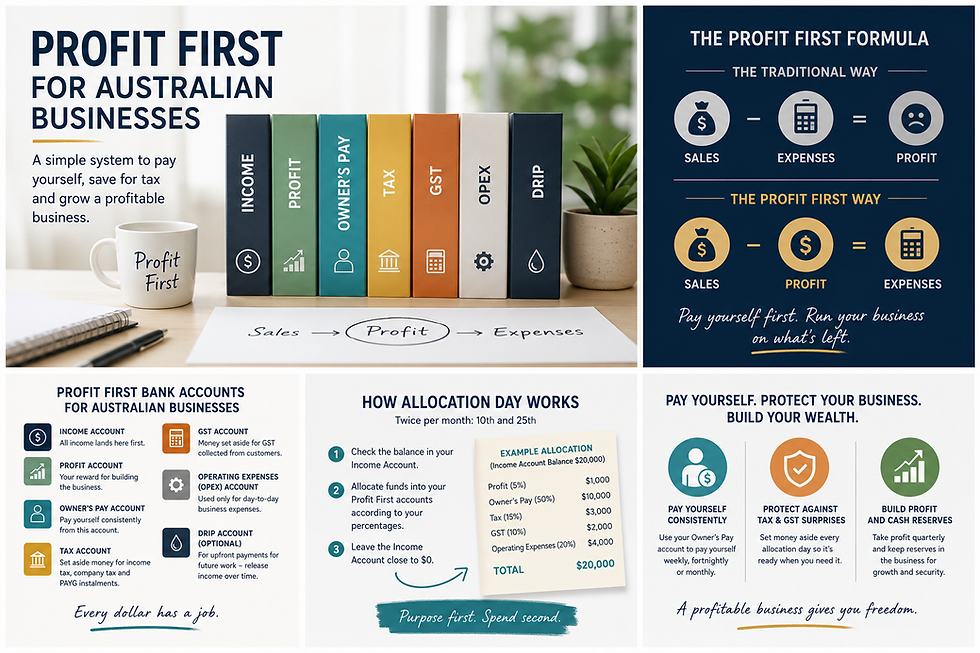

The reason is simple. Most businesses follow the traditional accounting formula:

Sales – Expenses = Profit

The problem is that profit becomes an afterthought.

Profit First flips this formula on its head:

Sales – Profit = Expenses

In other words, you take your profit first and run your business on what’s left.

This simple shift changes the way you manage money and creates a business that consistently pays you.

Here’s exactly how to set up and implement Profit First in an Australian business.

Step 1: Open Your Profit First Bank Accounts

For most Australian businesses, I recommend setting up the following accounts:

Income Account

Profit Account

Owner’s Pay Account

GST Account

Tax Account

Operating Expenses Account

Drip Account (optional)

Some businesses may also choose to have:

Superannuation Account

Payroll Account

Equipment or Capital Expenditure Account

What Each Account Does

Income Account

All business income lands here first. No expenses are paid from this account.

Profit Account

This account is your reward for building your business.

Owner’s Pay Account

This account is used to pay yourself consistently.

GST Account

This account holds the GST you’ve collected on behalf of the ATO.

Tax Account

This account holds money for:

Company tax

Personal tax for sole traders and partnerships

PAYG instalments

Fringe Benefits Tax (if applicable)

Operating Expenses Account

This is the only account used to pay the day-to-day expenses of running your business.

Drip Account

Perfect for businesses that receive large upfront payments for services delivered over several months.

Step 2: Remove GST First

One of the biggest mistakes Australian business owners make is including GST in their Profit First allocations.

GST doesn’t belong to you.

It’s money you’re collecting on behalf of the ATO.

Before you perform your allocations, transfer the GST component into your dedicated GST account.

For example:

Client payment received: $11,000 (including GST)

Transfer:

GST Account: $1,000

Remaining funds for Profit First allocations: $10,000

Your percentages are then applied to the $10,000, not the full $11,000.

This gives you complete confidence that your BAS obligations are already funded.

Step 3: Determine Your Allocation Percentages

Once GST has been removed, allocate the remaining funds according to your Target Allocation Percentages (TAPs).

An example for a service-based business may look like this:

Account | Percentage |

Profit | 5% |

Owner’s Pay | 50% |

Tax | 15% |

Operating Expenses | 30% |

These percentages are simply an example and should be tailored to your business.

The goal isn’t perfection on day one. The goal is progress.

Step 4: Deposit All Income Into the Income Account

Every dollar your business receives should first go into your Income Account.

The flow should look like this:

Client Payment → Income Account → GST Account → Profit First Allocations

Not:

Client Payment → Operating Expenses Account → Spend Whatever Is Available

This small change alone can transform the way you manage money.

Step 5: Allocate Money Twice Per Month

Profit First works best when you allocate money on a regular schedule.

The recommended allocation days are:

10th of the month

25th of the month

On these dates:

Check the balance in your Income Account.

Transfer the GST component into your GST account.

Allocate the remaining funds according to your percentages.

Leave the Income Account close to zero.

Example

Income received: $22,000 including GST.

Step 1:

Transfer $2,000 into the GST Account.

Amount remaining for allocations:

$20,000.

Step 2:

Account | Amount |

Profit (5%) | $1,000 |

Owner’s Pay (50%) | $10,000 |

Tax (15%) | $3,000 |

Operating Expenses (30%) | $6,000 |

Every dollar now has a purpose before it can be spent.

Step 6: Pay Yourself Consistently

Many business owners pay everyone except themselves.

Profit First changes that.

Your Owner’s Pay account should pay you:

Weekly

Fortnightly

Monthly

Choose a schedule and stick to it.

Avoid taking random drawings whenever money feels available.

Consistency creates certainty and helps separate your personal finances from your business finances.

Step 7: Build a Tax Buffer

Your Tax account is designed to cover:

Company tax

Personal tax

PAYG instalments

Fringe Benefits Tax

By setting aside money every allocation day, tax time becomes much less stressful.

Instead of wondering how you’ll pay your tax bill, you’ll already have the money waiting.

Step 8: Take Quarterly Profit Distributions

Every quarter, celebrate your success.

A common Profit First approach is:

Take a 50% distribution from the Profit account.

Leave 50% in the business as a reserve.

For example:

Profit Account balance: $8,000

Distribution to owner: $4,000

Business reserve: $4,000

These profit distributions remind you why you started your business in the first place.

Step 9: Use a Drip Account for Upfront Payments

If your business receives large upfront payments for services delivered over time, a Drip Account can be a game-changer.

For example:

A client pays $6,600 upfront for a six-month program.

Transfer:

GST Account: $600

Drip Account: $6,000

Each month:

Transfer $1,000 from the Drip Account into the Income Account.

Then perform your normal Profit First allocations.

This ensures you still have the cash available to deliver the service in the months ahead.

A Simple Profit First Account Structure

Income

├── GST

├── Profit

├── Owner's Pay

├── Tax

├── Operating Expenses

└── Drip (optional)Common Profit First Mistakes to Avoid

❌ Spending the GST you’ve collected.

❌ Including GST in your Profit First allocations.

❌ Mixing GST and income tax savings.

❌ Taking random owner’s drawings.

❌ Paying expenses directly from the Income Account.

❌ Forgetting to plan for future work already sold.

❌ Treating Profit First as just a bank account system instead of a behavioural change.

The Bottom Line

Profit First isn’t about complicated spreadsheets or cutting every expense.

It’s about giving every dollar a purpose and ensuring your business works for you, not the other way around.

Because a successful business isn’t one that generates revenue.

A successful business is one that consistently pays its owner, generates profit, and gives you confidence that there will always be money available for GST, taxes, and the future.

Because when you remove GST first and then allocate the money that actually belongs to your business, you finally start building a business that pays you first.

Comments